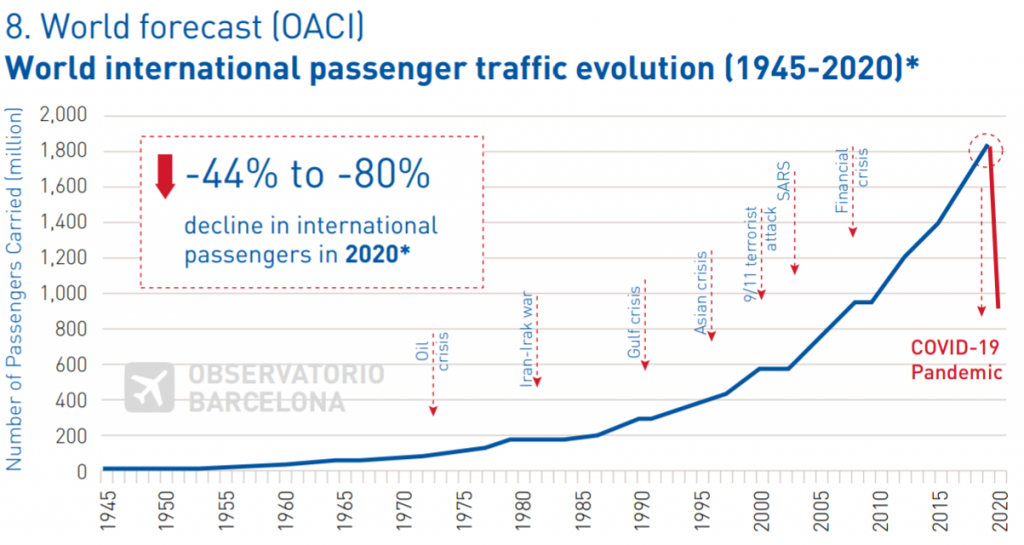

There are different perspectives for the recovery of air traffic given the severity of the COVID-19 health crisis and its economic consequences. According to different scenarios drawn by global sectoral agents, the crisis may take between 2.5 as optimistic or 5 years in the worst case compared to the 2019 level. For 2020, according to ICAO, a reduction between 44% -80 is expected. Percentage of international passengers globally (graph 8). Consequently, the world tourism sector could lose between 300 to 450 billion dollars in turnover due to the impact of the pandemic according to (UNWTO, graph 9). That implies returning to levels of 6 or 7 years ago.

The rate of recovery of the traffic that will go in parallel to the evolution of the disease will be asymmetric by regions or countries and will depend above all on 4 variables:

1. The liberalization of international passenger mobility. This will evolve unevenly according to the affected territories and countries. In general, especially domestic flights will be the first to recover as they have fewer restrictions.

2. Consumer confidence to travel: 40% of passengers according to a survey of IATA (April) will wait 6 months before traveling again as previously. It will also depend on the measures implemented by the companies, airports, and the destination in general (hotels, transport, etc.). to be agreed and implemented.

3. Business confidence: business demand will be restricted by cost adjustments in travel budgets and in some cases replaced by teleworking or general changes in their business models.

4. The companies’ restructuring capacity: there will be a reduction in the supply of flights and the number of companies, especially in Europe where there is a highly fragmented market. The essential part of this restructuring is the financing of its fixed costs while they do not operate and the investment necessary to start the activity, especially while demand does not recover and prices cannot rise. In this regard, those companies that have better protection from the states may enjoy some financial advantages. In an extrapolation of the IATA and ICAO perspectives for Europe and assuming that Barcelona behaves like the market average, two scenarios have been developed: the optimistic one with a reduction of -48% (compared to 2019) and the moderate one with a 74% reduction.

In an extrapolation of the IATA and ICAO perspectives for Europe and assuming that Barcelona behaves like the market average, two scenarios have been developed: the optimistic one with a reduction of -48% (compared to 2019) and the moderate one with a 74% reduction. In Barcelona this year is expected a passenger volume of 12.6 to 24.2 million O&D passengers (origin or destination Barcelona without taking into account passengers in transit, see graph 7).

Domestic flights are expected to be activated significantly between June and the beginning of July. This would be the biggest engine of activity this summer. As for European flights, it is foreseeable that it will start in an agreed way at the level of the European Commission and including other non-EU countries. It is difficult to estimate a date, but in any case, for the last quarter of the year, we should have certain normality. Intercontinental flights are not estimated to have a significant impact until summer 2021 (March-October).

Source: www.cambrabcn.org https://www.cambrabcn.org/documents/20182/51403/Observatori+37_maig+2020.pdf/b1fdd19b-c26d-009c-92ec-7c66b6e46c92