• 2021 has been a year of air recovery in terms of global air cargo demand, not only compared to 2020 but also compared to 2019. Specifically, in the Jan-Nov 2021 period, demand grew by +7.1 % (FTK, Freight Tonne-Kilometer) compared to the same period of 2019. This is not the case with the offer, which is still below 2019 (-13.4% AFTK, Available Freight Tonne-Kilometer), especially due to the lack of capacity in passenger flights (belly capacity).

• The demand recovery occurs in all regions, except Latin America, which still obtains negative results compared to 2019 (-16.3%). The region that stands out and leads the recovery is North America, which obtained +20% growth.

• According to Boeing forecasts, World air cargo traffic is expected to grow by +4.0% YoY over the next 20 years, in terms of RTK (Revenue Tonne-Kilometer). Therefore, the growth rate would slow down when compared to the average growth of +4.3% obtained during the 2009-2019 period.

•In a similar study by Airbus, forecasts a more moderate average annual growth (+2.7%), although both manufacturers agree on the leadership in terms of growth of the Express model motivated by e-commerce. Specifically, Airbus estimates the growth of this model at +4.7% YoY until 2040.

• The American manufacturer adds that, although wide-body passenger aircraft have contributed significantly to the growth of the air cargo industry over the last decade, freighters are expected to continue transporting more than 50% of World air cargo.

• BCN remains in the Top 25 European cargo airports, according to ACI and Eurostat data (Jan-Aug 2021 period). During this period, the Catalan airport grew by +15% compared to 2020, obtaining similar results to other comparable European airports (DUB, VIE, OSL).

• However, the growth of the large European cargo hubs (FRA, CDG, AMS, LGG) obtained higher growth, reaching up to +40% in the case of Liège (LGG). At the domestic level, ZAZ stands out, gaining several positions compared to the previous year thanks to the great growth obtained, while MAD remains in 11th place.

• The airports of the Aena network handled 998,000 tons in 2021, +26.5% YoY, although less than in 2019 (-6.6%). More than 50% was handled by MAD, which obtained +30% YoY, while BCN obtained +18.9% YoY. Neither of the two airports has recovered pre-covid levels, although Madrid airport is close.

• ZAZ and VIT, two airports specially oriented to the cargo business and therefore not affected by belly capacity reduction, both exceed 2019 results, obtaining +6.4% and +12.5% respectively

• Express/courier operators continue to lead the ranking of cargo airlines in BCN (DHL in 1st position and UPS in 3rd position). Amazon Air (through its aircraft leasing to ASL Airlines), is in 2nd position, and therefore confirms the great positive trend of e-commerce worldwide.

• Most of this cargo originates from or is destined for the European region (in its first segment), where the express operators have their main hubs (Leipzig, Cologne, etc.).

• Regarding traditional cargo airlines, Turkish Airlines leads the ranking (10.5% share), which overtakes Qatar (10.4%) and Emirates (7.1%).

• Derived from the impact of the health crisis on the traditional air cargo business in 2020, the express/courier model increased its market share at the airport, reaching 34.2%. In 2021, this indicator increased to 44.8%.

• This large growth is especially motivated by the great irruption of Amazon Air, which began to establish its triangular operations in BCN in 2021 (LeipzigBarcelona-Rome-Paris-Leipzig route). In the case of MAD, this operation follows the Cologne-Milan-Cologne-Madrid flow

• The first airport by origin or destination of goods handled in BCN was Cologne-Bonn (the hub of UPS and FedEx), despite the slight decline in cargo volume (-2.5% vs 2020).

• Instead, Leipzig/Halle rises to the second position, with an increase of +26.5% YoY, thanks to the triangular operation of Amazon Air. This triangular operation has allowed Rome to reach the 7th destination in the ranking (+355% YoY).

• Istanbul rises to 3rd place, surpassing Doha, in line with the trend of the airlines that operate these destinations (Turkish Airlines and Qatar Airways).

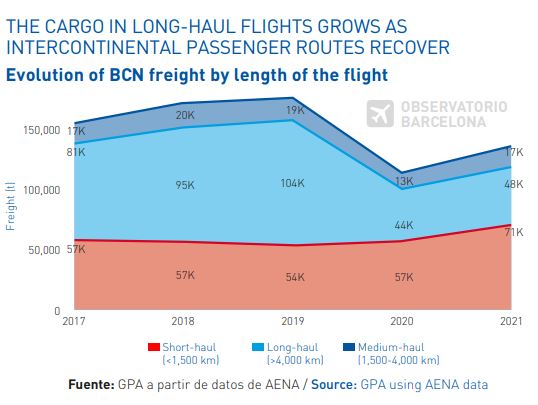

• The loss of intercontinental connectivity in 2020, which has continued with a progressive recovery of destinations during 2021, has meant that most of the air cargo in BCN has been transported on short or medium-haul flights (both in 2020 and in 2021), unlike what happened during the years before the pandemic.

• The return of important American routes during 2021 (such as New York, Miami, or Bogotá) has made it possible to have more belly cargo offer for distant destinations, a key aspect in this business. However, BCN still has to recover very important Asian connections that have transported large volumes in the past, such as Seoul, Shanghai, Beijing, and Hong Kong.

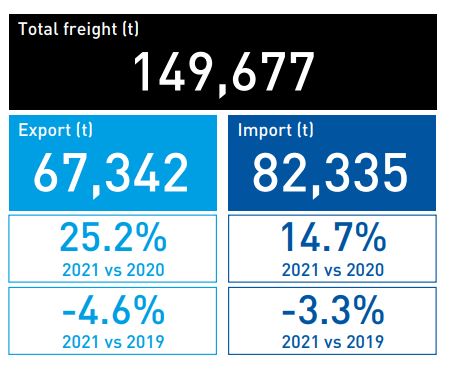

• During the Jan-Nov 2021 period, exports by air from Catalonia increased by +25.2% YoY. Imports did the same by +14.7%. The results compared to 2019 are -4.6% (exports) and -3.3% (imports), therefore being close to the pre-covid figures.

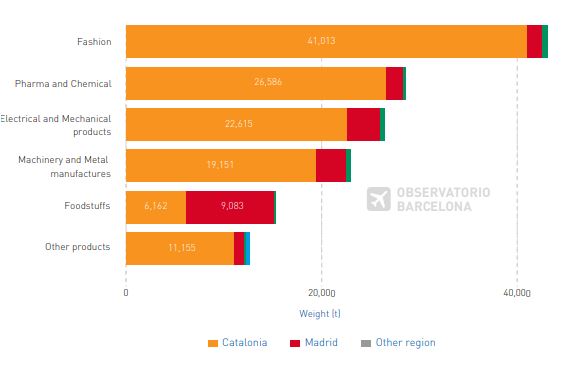

• Analysing the different sectors, the fashion sector obtains +20% YoY, although it is still far from recovering the 2019 results (-17.2%). The pharmaceutical sector obtained +4.6% compared to 2020 and +13.3% compared to 2019, being the only sector that has grown during the two consecutive years of the pandemic.

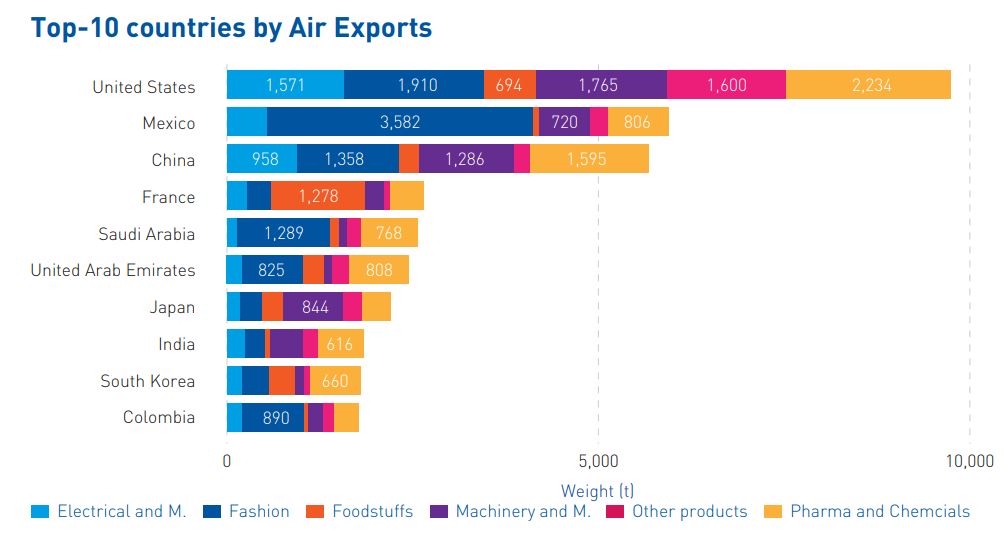

• In relation to the final destination of exports by air, the United States stands out (with a fairly even mix of products), Mexico (where the fashion product dominates), and China (also fairly balanced). Regarding imports, it is worth highlighting China (product mix), followed by Bangladesh (practically 100% fashion imports) and Germany (mainly electrical products).

• Most goods by air originated or with destination Catalonia arrive or leave through customs in the own region (more than 82% through Barcelona province).

• Madrid is the second region (in terms of customs) through which Catalan products leave or enter by air, although with much less share. However, it is worth highlighting the foodstuffs exported/imported by Catalonia by air, which mostly leaves or enter via customs in Madrid.

• More than 75% of the air goods inspected in Barcelona Customs have as their final destination or origin their own province.

• In terms of Barcelona Customs, its catchment area is very focused in Catalonia, although products from Madrid, Valencia, and Aragon are also handled.

• 56% of air goods inspected in Madrid Customs have as their final destination or origin their own province. In second place would be the products with an origin or destination in Barcelona (8.5%).

• In this case, the catchment area is more distributed than the Barcelona case, although mostly for imports.

• Air transport manages approximately 1%-2% of the total volume of goods worldwide, although in value this cargo represents a much higher share.

• In the case of Catalonia, goods by air represented 6.9% of the total value (€) of transported products, despite that they reached only 0.3% of the share in terms of weight. At the Spanish level, the value of air freight reached 8.8% of the total value of goods transported in 2021.

• The average value of goods transported by air in Catalonia in 2021 was 51.96 €/Kg. This indicator has followed a very positive trend in recent years, with the exception of this last year.

• The average value in other means of transport in 2021 reached 3.71 €/Kg by road, 1.95 €/Kg by rail, and 1.72 €/Kg by sea, following a stable trend in recent years.

• Analysing the average value of air cargo based on the flow, a very clear difference can be observed. While exports reached an average of 67.33 €/Kg during the 2020-2021 period, air imports obtained 40.27 €/Kg of average value.

• On the other hand, a great increase in value was produced during the worst months of the pandemic (March-April-May 2020). Probably the lack of ‘belly’ space due to the massive cancellation of flights (which caused a considerable increase in air rates), meant that the cost of air transport could only be assumed by the highest-value products.

Large differences are observed by sector. While the average value of pharmaceutical products reached more than 119 €/Kg in exports in 2021, for electrical products, machinery, or fashion, this indicator was between 41-61 €/ Kg for exports.

• In all cases, the average value of products imported by air is lower than those exported, although the greatest relative difference between both flows occurs in the pharmaceutical, fashion, and food sectors.

Source: GPA/Aena/MIDT

Produced by GPA www.gpa.aero